Your retirement should be secure, comfortable, and predictable, not uncertain. Our retirement calculator India is a retirement planning calculator that estimates your retirement corpus with inflation, acting as a smart retirement sip calculator and retirement savings calculator.

| Description | Value |

|---|---|

| Years in Retirement | |

| Inflation Adjusted Monthly Expense | |

| Required Retirement Corpus | |

| Accumulated Amount | |

| Shortfall | |

| Extra Monthly Saving Needed |

Retirement rarely arrives with a warning. It builds quietly over decades, shaped by small financial decisions. Yet most investors delay one crucial step, understanding how much they actually need.

A Retirement Planning Calculator changes that. It does not just project numbers; it translates your current lifestyle into a future requirement. And that shift in thinking often marks the beginning of serious retirement planning.

At a basic level, a retirement calculator estimates how much wealth you need by the time you stop earning. But the real value lies deeper.

A retirement planning calculator India factors in inflation, life expectancy, and expected returns. It answers the question many investors avoid: how much money do I need to retire? A simple retirement amount calculator may give you a number. But a detailed retirement calculator with inflation shows how rising costs silently reshape your future needs.

The hardest part of retirement planning is figuring out the final number. This is where a retirement corpus calculator, or a corpus calculator, becomes essential.

To find out how to calculate a retirement corpus, enter your current and retirement age, and your monthly expenses.

Choose an inflation rate and an expected return.

The retirement planning calculator India will then show the required monthly investment.

You can adjust inputs like tenure, return, or contribution to see how your retirement corpus calculator changes.

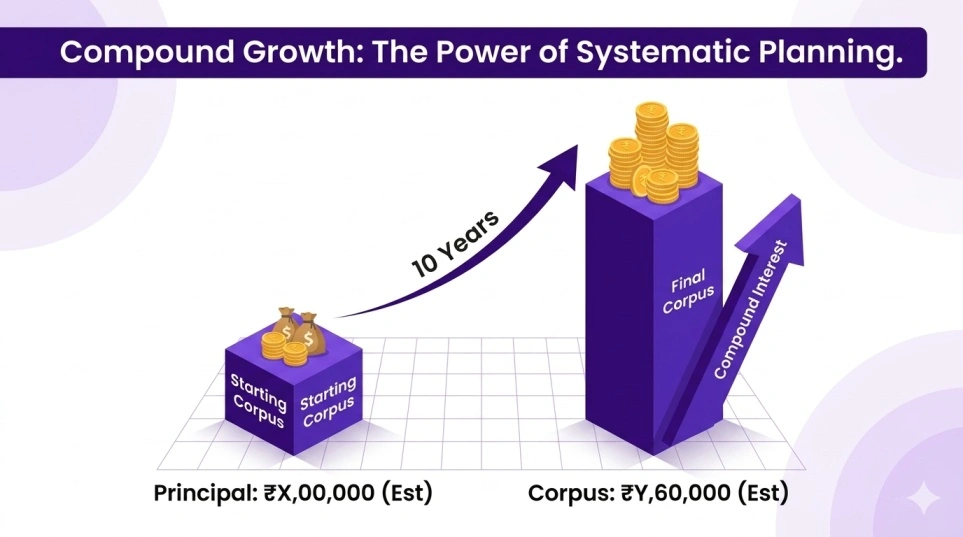

For example, if at age 30 your monthly expenses are ₹50,000, inflation at 6% can push them to nearly ₹2.9 lakh over 35 years. Thus, at the age of 60, you will have about ₹6.9 crore to fund your post-retirement expenses.

On the other hand, if you invest ₹6,000 during this period at an estimated return rate of 12%, you will accumulate a total of ₹2.1 crore. This would leave you with a shortfall of ₹4.8 crore. If you have additional savings, then deduct from this shortfall to estimate the final amount.

To bridge this gap and to cover your retirement expenses based on your current monthly expenditure, you would need to invest an additional ₹13,562 every month throughout this entire period.

This is also where investors start asking how much to save for retirement. The answer varies, but the method remains consistent.

In India, inflation is not a side variable. It is the core driver of retirement planning because inflation hovers over 6% realistically.

A retirement calculator India or retirement planning calculator India integrates inflation assumptions to show how purchasing power declines over time. This helps answer practical questions like how much money needed to retire in India.

The answer is often higher than expected, not because of lifestyle upgrades, but because of inflation alone.

Once the target is clear, the next step is execution. A retirement mutual fund calculator or retirement SIP calculator helps translate that corpus into monthly investments.

For instance, if your goal is ₹3 crore in 25 years, a retirement savings calculator can estimate the required SIP based on an assumed return.

This is where compounding plays a central role. Small investments made consistently over time can build significant wealth, especially when aligned with long-term goals.

Retirement is not just about accumulation. It is also about income.

A pension plan calculator or a monthly pension plan calculator helps estimate how much income your corpus can generate post-retirement.

For those relying on structured retirement plans, tools like a retirement pension plan calculator India or a mutual fund pension plan calculator can simulate withdrawal strategies.

This becomes critical when planning for stability rather than growth.

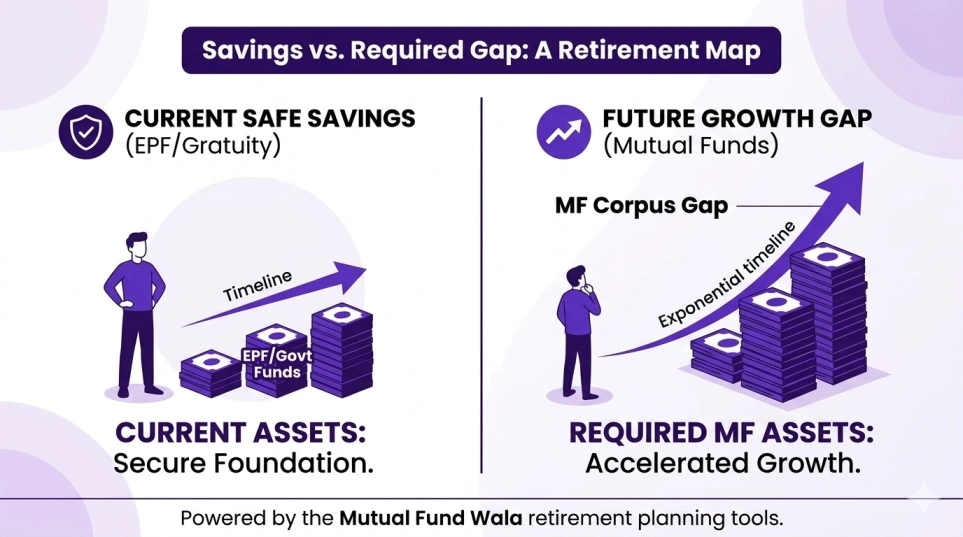

Many investors underestimate the role of existing retirement benefits.

An EPF pension calculator helps estimate a pension from EPF contributions. Similarly, a superannuation calculator projects employer-funded retirement benefits.

Investors also often ask how to calculate a pension after retirement and a retirement gratuity. These components, when added together, reduce the burden on personal investments. A well-structured retirement fund calculator should ideally account for all these sources.

This is the question every investor eventually faces: how much is enough for retirement calculator.

There is no universal number, but you generally need a corpus of 25-30 times your current monthly expenses to retire comfortably.

But a structured approach through a retirement calculator with inflation provides clarity.

For someone in their 30s, the required corpus may seem distant. But delaying action significantly increases the monthly burden. Starting early reduces pressure and allows compounding to do the heavy lifting.

This retirement calculator India works backwards from your target retirement goal and helps you:

If you already have savings or a pension plan, you can include them in this retirement savings calculator to see how much more you need to invest.

You can tweak numbers like tenure, return, or investment to see how your retirement corpus calculator changes in different scenarios.

This retirement fund calculator is for estimation only. Actual returns from mutual funds, EPF, or pension plans may vary with market conditions. Always review your plan and consult a qualified advisor before final decisions.

A retirement planning calculator by MutualFundWala does more than estimate numbers. It forces alignment between today’s spending and tomorrow’s needs.

It answers uncomfortable questions early, when there is still time to act. Whether you use a retirement SIP calculator, a pension plan calculator, or a retirement corpus calculator, the objective remains the same—clarity.

Because retirement is not built in the last five years of your career. It is built across the entire journey with MutualFundWala guiding your planning.

Ans: A retirement planning calculator helps estimate how much money you need to retire based on expenses, inflation, and expected returns.

Ans: It depends on your lifestyle, inflation, and life expectancy. Most calculators estimate this by projecting future expenses.

Ans: You generally need a corpus of 25-30 times your current monthly expenses to retire comfortably.

Ans: This depends on your target corpus and investment returns. A retirement SIP calculator can estimate the required monthly investment.

Ans: The amount varies widely, but inflation-adjusted calculations often suggest a corpus running into crores for urban lifestyles.

Ans: You can use a pension plan calculator or estimate your needs based on your corpus size and expected withdrawal rate.

Ans: It estimates pension income from EPF contributions based on salary and years of service.

Ans: Gratuity is calculated based on the last drawn salary and years of service using a fixed formula defined under the Payment of Gratuity Act.

Estimate your future savings and build a secure retirement plan today.

© 2026 MutualFundWala | AMFI Registered Mutual Fund Distributor | ARN-275889, Valid by 06-09-2026 | All rights reserved